scatteredRubbish

New Member

- 9

A few months back I posted on the forums questioning whether or not I should hold onto or dump a WL policy I have through NWM. After the advice given here, some fantastic podcasts I found exclusively on life insurance, and discussion with my adviser I have decided to hold on to the policy.

A lot of advice that was given to me was that I was not maxing out my policy and taking the fullest advantage of its cash value accumulation. I'm not sure what I can do to change this as that's key part of why I want a WL policy. A forum poster previously had mentioned internally changing the policy to an ACL policy and others said to add a PUA rider (which I think I already have? This just means by dividends go to paid up additions right?). I have a meeting scheduled with my advisor later this month to discuss some of this and I am looking to go into it with a bit more knowledge and information. I appreciate being able to get advice from experts here on a topic that can be challenging for your average consumer to fully grasp, so thank you all for that.

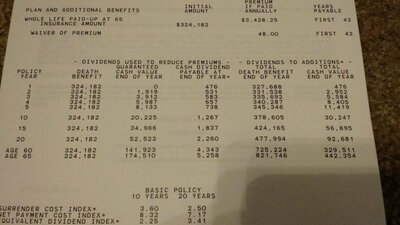

Attached is an image of my policy as it won't let me link to imgur without 20 posts.

A lot of advice that was given to me was that I was not maxing out my policy and taking the fullest advantage of its cash value accumulation. I'm not sure what I can do to change this as that's key part of why I want a WL policy. A forum poster previously had mentioned internally changing the policy to an ACL policy and others said to add a PUA rider (which I think I already have? This just means by dividends go to paid up additions right?). I have a meeting scheduled with my advisor later this month to discuss some of this and I am looking to go into it with a bit more knowledge and information. I appreciate being able to get advice from experts here on a topic that can be challenging for your average consumer to fully grasp, so thank you all for that.

Attached is an image of my policy as it won't let me link to imgur without 20 posts.