No offense taken.

If a policy is over 7 years old a face amount reduction generally will not cause a MEC.

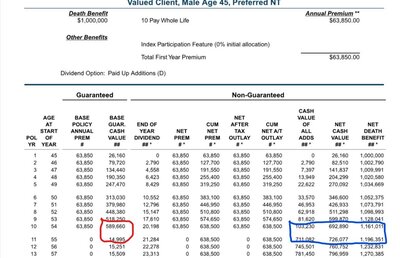

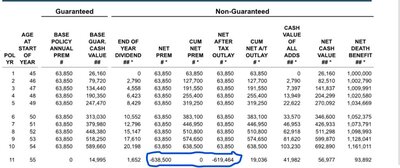

This is a male 45 face amount reduce to minimum non mec.

The adds bought enough face that the net db did not change much.

Being I am retired and have too much time on my hands Imdecided to play around with this.

A few months back we had a thread regarding recapture ceilings.

I tried to generate an illustration showing one but could not.

So I did a face reduction and a withdrawal in the same year and voila!

Have a great weekend!

One last thought..........a long one But there should be a disincentive from borrowing. Dividend crediting SHOULD be LESS than loan rates. In theory I agree

Look at this from the perspective of a mutal company.

All policy holders should be treated fairly and equally.

Years ago interest rates were above 10%.

If your loan rate was 8% you could borrow from your policy and invest it in a cd and create an arbitrage not accounting for taxes.

That is when Direct Recognition payed a lower dividend on borrowed money, as your loan was an asset of the general account, the insurance company was receiving interest at a lower rate than what they could invest for,

In essence the non borrowers where subsidizing the borrowers.

Direct Recognition fixed this.

Let's fast forward to today.

If a company has a loan rate of 6% and you borrow your money that loan is yielding more interest than current investments in the General Account.

In order to keep things equal it is only fair to give borrowers a higher dividend.

In 30 years I have found one thing that I know is true.

Insurance companies have enough data and enough actuarial brainpower to know that long term there is probably no difference between Direct Rec or Non Direct Rec.

At any given time one is better than the other. It's a non issue as a selling point.

If your client wants to borrow money, let him go to a third party lender and take out a cash value loan.

I does not effect the polict and the client is forced to pay the principle and interest.

I'm outta here!

Let me ask a comparable question in a different way with a different product:

If you had an annuity with a guaranteed lifetime withdrawal feature for 5% (just making up a number) and you pull out more than 5% in any given year... does the policy reflect that you can do that? (Actually it does because you can take the withdrawal. Over 5% but under 10% of the free withdrawal amount means you can without a surrender charge, but your lifetime benefits will be recalculated. If you take out over 10%, the amount over 10% will be subject to a surrender charge.)

Is the re-calculation of benefits stated in the annuity policy? No.

Will a re-calculation happen? Yes.

Would it be stated in the policy that a recalculation would happen? Yes.

Will it be for the policyholder's advantage? Most certainly not.

So, using that analogy, we can do the same with whole life insurance.

Can you make a withdrawal of available cash values? Yes and at any time.

Will it create a re-calculation (reduction) of death benefits? Yes.

Do we know how much the re-calculation will be? No.

Is it for the benefit of the beneficiaries? Most certainly not.

That is not the same. Annuity features are based & triggered on the payments/deposits. Those life withdrawal guarantees are a function of the cash value. WL base policy face amount is a selected stated guaranteed face amount, it isn't a reflection of the premiums/deposits.

Unless contractually stated that it can be modified, WL face amount will stay exactly the same face amount. Unless partial withdrawals of base CV are contractually stated, they won't be allowed.

UL chassis products have such specific contractual language about face reductions & partial withdrawals

In order to keep things equal it is only fair to give borrowers a higher dividend.

In 30 years I have found one thing that I know is true.

Insurance companies have enough data and enough actuarial brainpower to know that long term there is probably no difference between Direct Rec or Non Direct Rec.

At any given time one is better than the other. It's a non issue as a selling point.

If your client wants to borrow money, let him go to a third party lender and take out a cash value loan.

I does not effect the polict and the client is forced to pay the principle and interest.

I'm outta here!

That is not the same. Annuity features are based & triggered on the payments/deposits. Those life withdrawal guarantees are a function of the cash value. WL base policy face amount is a selected stated guaranteed face amount, it isn't a reflection of the premiums/deposits.

Unless contractually stated that it can be modified, WL face amount will stay exactly the same face amount. Unless partial withdrawals of base CV are contractually stated, they won't be allowed.

I'm looking through my CLU text and I saw this: "The policyowner's investment can be withdrawn at any time with no loss of cash value unless surrender charges apply. This can be accomplished through surrender for cash or through policy loans."

Of course, surrender for cash means giving up the entire policy, not just a partial withdrawal.

So, now that I'm thinking about it... I think I learned that you could withdraw from your policy from MassMutual because of the flexibility of their Legacy 100 series contracts?

MassMutual did some interesting things with their policies so you could make adjustments to THAT policy - including increasing coverage (pending underwriting) and taking a withdrawal that would then reduce death benefits permanently.

So I'll say that my assertion... may very much be company & policy specific. And since that was about 15 years ago... it's possible that I may have even misheard it back then too.

I'm looking through my CLU text and I saw this: "The policyowner's investment can be withdrawn at any time with no loss of cash value unless surrender charges apply. This can be accomplished through surrender for cash or through policy loans."

Of course, surrender for cash means giving up the entire policy, not just a partial withdrawal.

So, now that I'm thinking about it... I think I learned that you could withdraw from your policy from MassMutual because of the flexibility of their Legacy 100 series contracts?

MassMutual did some interesting things with their policies so you could make adjustments to THAT policy - including increasing coverage (pending underwriting) and taking a withdrawal that would then reduce death benefits permanently.

So I'll say that my assertion... may very much be company & policy specific. And since that was about 15 years ago... it's possible that I may have even misheard it back then too.

I think it could be a great design, just havent seen contract language allowing it. I am sure the actuaries know if it is too flexible on the base policy, people could keep them. Part of the long term profitability design is that some will lapse, some will auto premium loan & some will go RPU which all tend to be better for long term profitability