- 656

Link below to Leslie Scism's Aug. 29 Wall Street Journal article about New York Life pitching a new "simplified" LTC product to middle market...

Couple of excerpts:

New York Life Insurance Co. is trying to find a new way to sell a product that some middle-class customers don’t want to buy anymore.

The company said it recently started offering a simplified version of long-term care insurance that makes the coverage easier to understand and more predictable in cost...

The new offering from New York Life is one of very few long-term-care policy introductions of the past five years, according to insurance-industry organizations, consultants and academics. It is designed to appeal to middle-class consumers. The longtime seller of such coverage will continue offering its existing stand-alone product...

The new policies from New York Life will generally cost at least $100 to $150 a month per person, depending on age and designated benefit level. As much as $500,000 in future payouts for a couple is available. The cost will generally be in the midrange of top-selling products, according to industry figures.

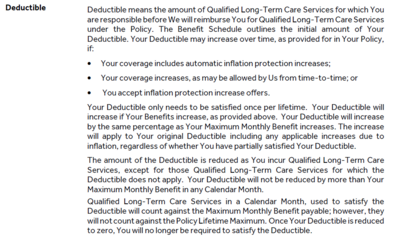

The insurer is scrapping use of “elimination periods,” which are typically 90-day waiting periods before the policies pay out. Instead, it is using a one-time deductible. A deductible is a specified amount of money that a policyholder is responsible for paying.

The “elimination period” concept can be off-putting to consumers because the amount they would need to pay isn’t known when they are purchasing a policy.

New York Life Tests New Pitch for an Unpopular Insurance Policy

Couple of excerpts:

New York Life Insurance Co. is trying to find a new way to sell a product that some middle-class customers don’t want to buy anymore.

The company said it recently started offering a simplified version of long-term care insurance that makes the coverage easier to understand and more predictable in cost...

The new offering from New York Life is one of very few long-term-care policy introductions of the past five years, according to insurance-industry organizations, consultants and academics. It is designed to appeal to middle-class consumers. The longtime seller of such coverage will continue offering its existing stand-alone product...

The new policies from New York Life will generally cost at least $100 to $150 a month per person, depending on age and designated benefit level. As much as $500,000 in future payouts for a couple is available. The cost will generally be in the midrange of top-selling products, according to industry figures.

The insurer is scrapping use of “elimination periods,” which are typically 90-day waiting periods before the policies pay out. Instead, it is using a one-time deductible. A deductible is a specified amount of money that a policyholder is responsible for paying.

The “elimination period” concept can be off-putting to consumers because the amount they would need to pay isn’t known when they are purchasing a policy.

New York Life Tests New Pitch for an Unpopular Insurance Policy