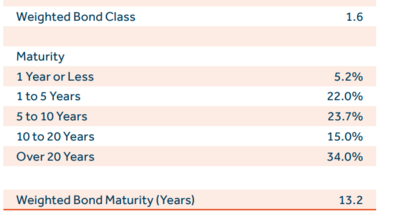

The interesting part to me is that carriers tend to brag about liquidity & many agents point to standards comparative report & liquidity.

If so much is tied up in long term bonds & so little matures/expires each year, how is so much of it considered "liquid". Sure, they can sell at a loss or prior to maturity, but i think most agents misunderstand "liquid", possibly myself included to some extent

The interesting part to me is that carriers tend to brag about liquidity & many agents point to standards comparative report & liquidity.

If so much is tied up in long term bonds & so little matures/expires each year, how is so much of it considered "liquid". Sure, they can sell at a loss or prior to maturity, but i think most agents misunderstand "liquid", possibly myself included to some extent

If you actually studied liquidity at Commercial banks, you would not leave any money in your checking account. Frankly, if it weren't for the Federal Reserve promise to bail out and Feds ability to print unlimited money, they would not survive. Why do you think Banks and Insurance companies always show large buildings in ads, even though its all mortgaged to the last penny. Insurance companies are not legally backed by the Fed. However, if there was a large run on insurance companies, they would flood the market to sell Government bonds and trust me Fed wont stay silent. Also we have seen what happens in cases like 9/11. People dont go out and cancel life insurance plans in a hurry, but they may hit ATM's. There is something psychological about having a policy of 300k cash value and 500K death benefit. When I cash it out, in my head I may feel my children will receive 500k less.

In 2022 I received a dividend of 112% of my premium. This generated Paid Up Additions of 148% of my premium.

(There is a note in the dividend box of the 2021 information sheet that says the dividend scale for the policy has changed. There was a similar note in 2019. Don't have other sheets to check in that file folder right now.)

MLSDev stands as a trailblazer in the realm of technology for warehouses, driving innovation and efficiency across the supply chain. As warehouses increasingly become hubs of technological integration, MLSDev's contributions play a crucial role in shaping the future of warehousing and logistics. https://mlsdev.com/services/mobile-app-development By leveraging cutting-edge solutions, businesses can transform their warehouses into agile, tech-driven ecosystems that meet the demands of today's dynamic market. As technology continues to evolve, MLSDev remains at the forefront, enabling warehouses to embrace the full potential of technological advancements in their quest for operational excellence.