Do those other carriers have a 4.98% or 7.5% design charge.

Honest question, in a flat year on $100k cash value, does this mean a client could would see their following anniversary be at $92,500 because of the 7.5% design charge in addition to whatever the annual COI charges are?

Yes, that is exactly what would happen. And if the S&P is up 100% in 5 years then the $100k becomes $370k. I'm 28 I like my chances of compounding at an average 9% tax-free better than having to stock pick or fund an IRA. Even without leverage, the 5 year index never had a return of less than 45% over 5 years since 2009. I don't mind taking a few negative months if the long-term trend is up. But you could always take away the multiplier at your anniversary.

Ah. I thought you were talking about an internal charge in the policy.

Yes. That is the charge for those riders.

7.5% deduction in index return to get a 2.7x multiplier.

4.98% deduction in index return to get a 2.14x multiplier.

The multiplier is not guaranteed and can be reduced to 1x at any time.

All the sales material Ive seen for this does not show how the index would have performed during the 80s/90s/early 2000s. They only show the largest bull market in US history.

Oh... and the participation rate on the index is not guaranteed.

Its not guaranteed and costs 7.5%.... and somehow Pac is able to spin this as a positive.... LMAO!!

You're wrong on both points. The participation rate is guaranteed at no less than 100% and the performance factor by default is 1.0 which means nobody has to EVER use the multiplier if they don't want to. It's just nice to have access to a GUARANTEED minimum of 170% of the uncapped S&P 500 index over 5 years guaranteed at no less than 105% participation rate.

Wow. I cant get over that Pac Life index switcheroo. What a FU to policy holders!!

Ive seen and heard about some sh*t in this industry. But SUPRISE, WE ARE CHANGING YOUR 0% FLOOR POLICY AND NOW YOU ARE AT RISK OF A 7.5%+ LOSS EACH YEAR!

Happy 2023!!

What a horrible thing to do to policy holders.

That is a guaranteed class action suit. Write it down, mark my words.

Allen needed a magnifying glass to see that fine print about a 7.5% Fee!!

They haven't taken anything away. Where did you get that idea? They are coming out with a new Pac Life Horizon product and this new Volatility Controlled index is being added to in-force policyowners.

Here is my current in-force policy showing the new indexed accounts and guaranteed participation rates and guaranteed 45 basis point return even if the Blackrock index is negative and you don't use any multipliers.

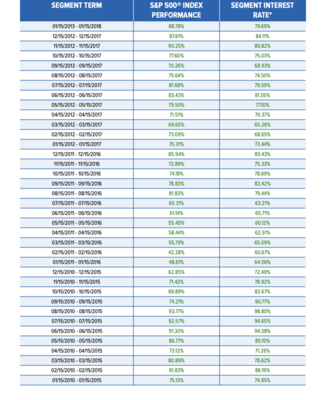

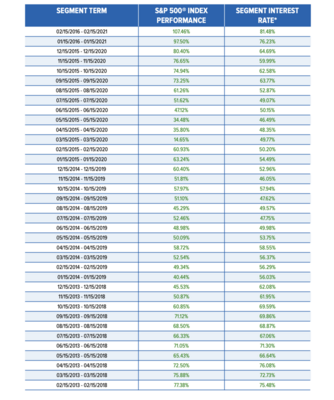

Yes, that is exactly what would happen. And if the S&P is up 100% in 5 years then the $100k becomes $370k. I'm 28 I like my chances of compounding at an average 9% tax-free better than having to stock pick or fund an IRA. Even without leverage, the 5 year index never had a return of less than 45% over 5 years since 2009. I don't mind taking a few negative months if the long-term trend is up. But you could always take away the multiplier at your anniversary. View attachment 8357View attachment 8358

Of course not, because that is the start of one of the longest bull markets in history (bolded).

That being said, at 28 and knowing the risks, maybe not a bad way to take a flyer on a portion of your portfolio. I wouldn't buy this thing since IUL will still perform more like a bond over the long term (in performance, not correlation) than a stock and I don't want my bonds to have this much risk.

Is this from the 5 yr pt to pt. In your other post showing the 5 year from 2009 to present posted 70-90% for a 5 year period, how does 100k become 370k in 5 years at annual averages of 15-18%. Still a great return, but wouldn't 100k become closer to $190k. Or are you saying the multipler on top of it would further drive it to $370k

Also, wouldn't the 5 yr average cost of the 5 yr pt to pt have an average deduction of 37% for the cost of the multiplier rider?

Lastly, if the insurance compamy could consistently turn 100k into $370k with all their billions in surplus, they would have zero need to have new policy sales to attract money that is very costly up front to acquire & to carry the liabilities & reserves of death claims. If this product design isn't more profitable to the carrier than a standard design of other carriers, I would think they would just go all in with their cash to hold the bonds & options in their own portfolio rather than using those financial benefits for the max gains of the consumer

You're wrong on both points. The participation rate is guaranteed at no less than 100% and the performance factor by default is 1.0 which means nobody has to EVER use the multiplier if they don't want to. It's just nice to have access to a GUARANTEED minimum of 170% of the uncapped S&P 500 index

I'm 28 I like my chances of compounding at an average 9% tax-free better than having to stock pick or fund an IRA. Even without leverage, the 5 year index never had a return of less than 45% over 5 years since 2009. I don't mind taking a few negative months if the long-term trend is up.

Agree, could be great to supplement to other retirement plans. However, life insurance cash values are not compounding tax free. They are technically compounding tax deferred. The only part tax free is your cost basis or if you die, the death benefit.

The gains in the policy are indeed taxable if you receive them. Now, if you want to let the insurance company or another bank become the collateral owner of the policy, you can borrow their money & pledge your policy as collateral. Their loans of their money to you are not taxable as you receive loans from them. But the ledger of your ever-compounding loan balance is still entirely taxable (both the loans & the loan interest) unless you die. I have witnessed many consumers get massive tax bills in this exact scenario.

At 28 & myself 53, we believe we will remember all this minutae when we are 80, 90, 105.....but we won't & there will likely be zero people at the carrier or an agent at the time making sure we don't do something stupid & only regret it at tax time 5-18 months later.

At 85, someone getting an anniversary statement showing their Cash value of $2M now has a surrender value of $10k will likely call to surrender. Others may lapse of overload protection not involved or deemed illegal by IRS. Others may have ignorant or greedy agents come in & unknowingly 1035 exchange the policy & trigger the loan being extinguished & causing massive tax bill.

If I was you, I would mix it up & make sure you are utilizing some other Qualified, Roth or after tax funds. While these plans can have some losses, they don't have caps & most of all they don't have 3-4 layers of expenses tied to a life policy to overcome.

My belief is all of these are good in moderation & no single one is the golden goose. Plus, can you imagine if a carrier fails or changes course 180 degrees & you have everything in one place. 70-90 years is a long commitment to think some won't go out of business or others won't gut their product. In my 25 year career, seen some carrier failures, but seen 5-10 larger carriers completely stop selling life insurance & then heavily impact inforce business in higher COI, worse interest or dividends, etc